China’s Economic and Strategic Relations with the Levant Region – Nader Habibi

DOI: 10.13140/RG.2.2.34332.62085

E-ISSN: 2718-0549

For more than a decade, the US administrations have tried to reduce their engagement in the Middle East and North Africa (MENA) to focus more on containing China in the Indo-Pacific region. However, this might prove a futile strategy because China has been busy during the same time interval deepening its presence in the Middle East. It has expanded its economic and strategic relations with the US allies and adversaries alike. This rapid expansion of China-MENA relations might force the United States to remain engaged in the region. However, the terms of US engagement with the Middle East are likely to change because China is more after economic interests than military presence or geopolitics.

Most scholars that study China’s expanding economic relations with the Middle East focus on her relations with the oil-exporting MENA countries such as Iran and Saudi Arabia. This focus is justified by China’s high demand for oil and natural gas in the past three decades. As a result, many studies have been conducted on China’s relations with the oil-exporting countries of the Persian Gulf, particularly the Gulf Cooperation Council and North Africa. Yet as I will demonstrate in this report, China has also made a solid effort to expand its relations with the Levant region of the Middle East, which is not a significant source of energy resources. The Levant countries included in this study are Egypt, Israel, Iraq, Jordan, Turkey, and Syria.

China’s interest in Levant countries is motivated by economic and strategic factors other than oil. Yet, most of these motives fall within the broad framework of its global strategy known as the Belt and Road Initiative. This report will analyze the evolution of China’s economic relations with the Levant countries in recent years. In my analysis, I will first focus on the unique features of China’s bilateral relations with each one of them. Then I will try to shed light on the common characteristics of China’s relations with these countries and ask if there is a common denominator in China’s economic ties with Levant that sets this MENA subregion apart from other subregions as the Gulf Cooperation Council.

Trade

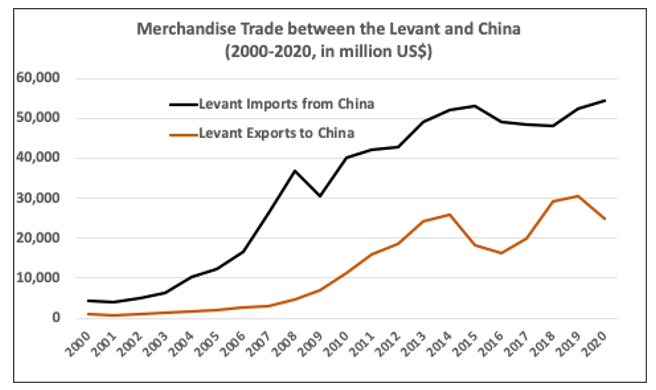

For more than four decades, China has served as the manufacturing hub of the global economy, and in recent decades it has also managed to produce advanced technological products at highly competitive costs. As a result, it enjoys an advantage in exports of a wide range of manufactured goods compared to other industrial countries. The Levant countries imported $4.2 billion worth of goods from China in 2000, while their combined exports amounted to $1.05 billion. Twenty years later, the value of Levant’s imports and exports with China in 2020 was sharply higher at $53.4 billion and $24.9 billion, respectively. Along with this sharp increase in bilateral trade, China’s rank among the Levant countries’ trade partners has also increased significantly. In recent years China has become the largest source of imports for Egypt, Israel, and Lebanon while reaching the second rank for Turkey, Syria, and Jordan. It ranked third among Iraq’s import origins after the UAE and Turkey. China did not rank high for most levant countries as an export destination except for Israel (advanced machinery, 2nd) and Iraq (crude oil, 1st).

Figure 1: Merchandise Trade between the Levant and China

Source: IMF, Direction of Trade Statistics, the regional aggregate calculated by the author.

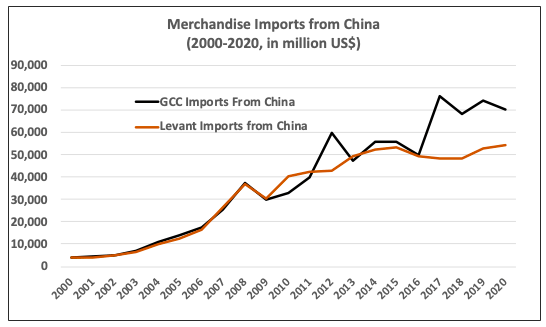

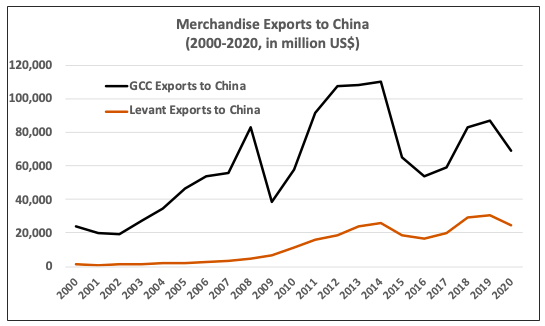

All levant countries, except Iraq, have experienced large trade deficits in their trade of merchandise goods with China. As shown in Figure 1, the region as a whole has consistently experienced a trade deficit with that country. The Levant region’s trade experience with China is not significantly different from other emerging regions. As demonstrated in Figure 2-a and Figure 2-b, the GCC countries’ imports from China have followed a similar trend as the Levant. Still, we observe a divergence in their export trends explained by GCC’s significant oil and gas exports to China. Unlike the Levant, the GCC countries have enjoyed large trade surpluses with China in most years since 2000.

Figure 2-a: Merchandise Imports of Levant and GCC from China

Source: IMF, Direction of Trade Statistics, the regional aggregate calculated by the author.

Figure 2-b: Merchandise Exports of Levant and GCC to China

Source: IMF, Direction of Trade Statistics, the regional aggregate calculated by the author.

Investment

Another critical dimension of economic relations between two countries is foreign investment. As a result of its massive trade surplus with the rest of the world, China has emerged as the leading international investor and creditor of large-scale projects. Initially, most of China’s foreign investments in developing countries were concentrated in mining and associated industries to facilitate the production and transportation of energy supplies and other raw materials to China[i].

Now China uses the Belt and Road Initiative (BRI) to guide its global investment and lending strategy. The BRI represents China’s vision to promote international trade and investment globally under Chinese leadership and primarily with Chinese credit. According to this vision, China supports the development of highways, railroads, and commercial seaports throughout the world with a priority in Asia, the Middle East, and Africa. The main objective is to facilitate trade and connectivity between China and the countries that join the BRI on the one hand, and among these countries, on the other.

In this context, China is actively supporting the development of transportation infrastructure in Central Asia and Eastern Europe to facilitate land trade and tourism with this region and with Western Europe and the Mediterranean. Well aware of this Chinese objective, Turkey has actively campaigned to position itself as one of the multiple east-west transportation corridors that China is developing for this purpose. This campaign has been successful, and in recent years China has financed several large-scale railway and road projects in Turkey.

Other Levant countries have been less suitable for BRI land transportation projects for two reasons. First, the multiple tensions and conflicts among Levant countries reduce the feasibility of cross-border transit routes. Israel, for example, remains highly isolated from its Arab neighbors because of the ongoing Palestinian conflict. Turkey’s relations with the Arab Levant countries and the relations among these countries have become highly unstable and contentious after the Syrian civil war. As a result of these adverse factors, China is investing in developing commercial seaports for BRI connectivity in these countries.

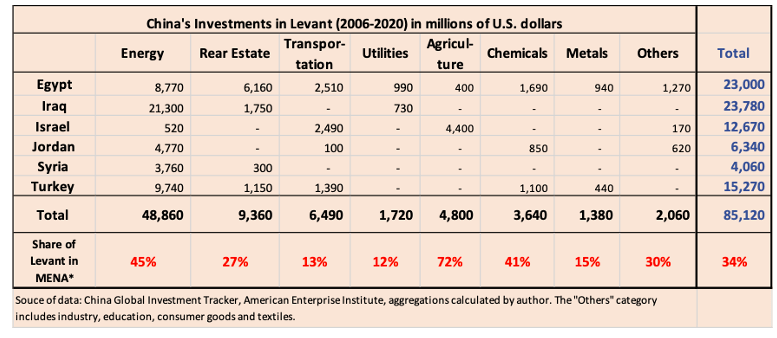

Table 1: China’s Investments in Levant

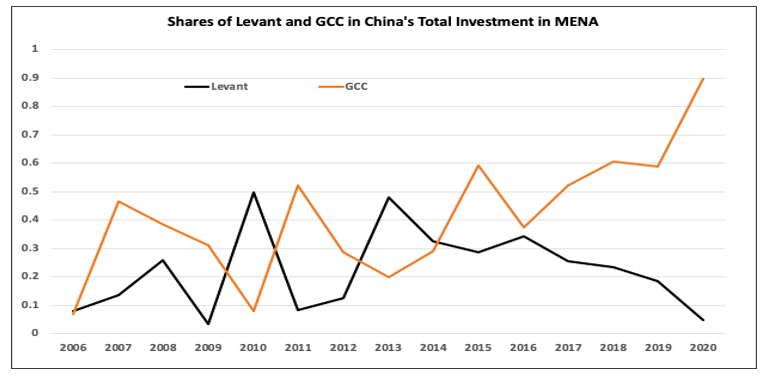

China’s investment pattern in Levant countries since 2006 is reported in Table 1. We observe that during 2006-2020 China has invested $85.1 billion in the six Levant countries reported in this table. This figure amounts to 33% of China’s total investment ($251 billion) in the MENA region during the same period. In comparison, the GCC received 40% of China’s total investment. The shares of Levant and GCC regions in China’s total investment in the Middle East region enjoyed a positive uptrend between 2006 and 2016, but they diverged after 2016 (Figure 3). While the share of GCC continued to increase, the percentage of Levant countries declined. This divergence was also associated with a sharp decline in China’s total investment in the MENA region (and the rest of the world) due to the Covid-19 pandemic.[ii]

Figure 3: Shares of Levant and GCC in China’s Total investment in the MENA

Source: American Enterprise Institute, China Global Investment Tracker, the regional aggregates calculated by the author.

Bilateral Relations:

Egypt: Among Levant countries, Egypt received the largest share of Chinese investments even though Turkey has a larger economy. China’s investments in Egypt are very diverse and are spread among many sectors (Table 1). This diversity reflects Chinese firms’ interest in using Egypt as a manufacturing and export center for access to European and African markets. Furthermore, the Egyptian government has shown a solid commitment to creating a hospitable investment environment for Chinese firms.

The bilateral economic relations between the two countries go back to the Hosni Mubarak era, and they have proven durable despite the two regime changes in Egypt since the Arab Spring.[iii] Good relations with Hosni Mubarak did not prevent China from developing close ties with President Mohammed Morsi, who was elected after the 2011 Arab Spring Uprisings. Similarly, China’s good relations with Morsi not only did not disrupt China’s relations with Egypt after the Egyptian army toppled him, but President El-Sisi expanded the bilateral economic ties even further. This durability is essentially a result of China’s non-intervention and non-interference policy in Egypt’s domestic political affairs, which stands in sharp contrast with interventions of the United States, Turkey, and many European countries.

China’s economic relations with Egypt have expanded rapidly since the military coup that brought President El-Sisi to power and ended the Arab Spring’s political instability. China is now the leading foreign investor and engineering contractor for Egypt’s new administrative capital under construction 45 kilometers east of Cairo.

Further to the east of the new administrative capital, China is the primary developer of Egypt’s Suez Canal Economic Zone (SCEZ). The Egyptian government’s long-term economic strategy calls for the transfer of industrial activity and attraction of foreign investment to this economic zone, which will have easy access to global markets through the Suez Canal. In addition to being active throughout SCEZ, China has developed a special area of the zone into a designated area for Chinese firms and modeled it after the Tianjin Economic-Technological Development Area (TEDA) in northeast China. Accordingly, this China-Egypt economic zone is called the TEDA-Suez Economic and Trade Cooperation Zone[iv]. More than one hundred Chinese industrial and logistics firms are already active in the TEDA-Suez zone, including the world’s largest fiberglass producer, the Jushi Industries[v].

These massive Chinese investments in Egypt reflect the Chinese government’s desire to incorporate Egypt in the Belt and Road Initiative as a regional logistics and manufacturing hub for trade with Africa and the Mediterranean regions. As such, Egypt has a higher priority for China than other Levant countries. Indeed, the rapid expansion of China-Egypt economic relations can come at the expense of China-Turkey relations. It might even reduce the significance of Greece and Israel in the Belt and Road Initiative. Many Chinese firms are now setting up their regional hubs in Egypt. This will reduce their need for establishing regional centers in Turkey, which is the most significant potential rival to Egypt for China’s attention.

Turkey: In recent years, China has also shown a strong interest in Turkey, which has faced several American and European economic sanctions and, on two occasions, has been vulnerable to currency depreciation crises. Yet, on both occasions, China’s timely injection of investments and loans has helped alleviate the situation and prevent a sharp devaluation of the Lira. In Summer 2018, for example, when the escalation of diplomatic tensions between Turkey and the United States caused a 40% decline in the exchange value of the Lira. China helped Turkey support its national currency by offering her a $3.6 billion loan for infrastructure projects.

Although we might expect the bulk of China’s investments in Turkey to be concentrated in the BRI-related transportation infrastructure projects, more than 60% of them ($9.7 billion) during 2006-2020 were made in the energy sector- primarily coal-powered plants. Indeed, China’s biggest investment project in Turkey is the 1.3-Megawatt Hunutlu EMBA coal plant in the Adana Province. This emphasis on energy is partly a result of the Turkish government’s strong interest in such plants, which can utilize the domestic supplies of coal. Progress of some of these projects has been slower than expected, and they have been criticized for pollution and environmental concerns. While the Turkish government has shown a strong commitment to these China-financed power plants, Turkish environmental NGOs pressure China to switch from coal-powered plants to renewable energy plants (wind and solar) in Turkey. China has already invested in two renewable projects in Turkey.

After these energy projects, the other large Chinese projects in Turkey are transportation infrastructure mega-projects such as the Yavuz Sultan Salim Bridge in Istanbul and the Kumport seaport terminal. China has also agreed to finance the Istanbul Canal, which will serve as an alternative to the Bosphorus canal for access to the Black Sea. This project has proven highly controversial and contentious in Turkish domestic politics because of environmental concerns. In addition to strong condemnation by opposition parties and environmental scientists, the Turkish domestic banks and European banks have also refused to offer financing for this project. Several Chinese banks stepped forward to fill this void, and President Erdogan officially inaugurated the Istanbul Canal project in June 2021.

Unlike in Egypt, China’s investments in Turkey are not concentrated in a small number of industrial zones (equivalent to the Suez Canal Economic Zone). This is partly because fewer of these projects are in manufacturing, and Chinese real estate projects such as hotels and resorts are dispersed throughout the country. The Turkish government is encouraging China to increase its manufacturing investment in Turkey, and some progress has been made in textiles, electronics, and telecommunication. China’s two giant telecommunication firms, Huawei and ZTE, are active in Turkey’s telecommunication industry. Huawei is developing Turkey’s 5G telecommunication network, and it has also established a large research and development center in Turkey. ZTE has purchased a majority share in Turkish electronic firm NETAS and is producing a diverse set of telecommunication and internet products and services.

Both of these ventures represent China’s high-tech and advanced technology partnerships with Turkey. Although Chinese technology and expertise are dominant in these partnerships, the Turkish economy has achieved a degree of advancement in these sectors that its participation is not limited to the one-sided adaptation of Chinese technology. Instead, some level of partnership in research and development and joint production of high-tech products is visible. For more labor-intensive and low-technology products, Turkey is likely to face intense competition from Egypt to attract Chinese investment, as will be described later.

Israel: China’s third-largest economic partner in the Levant is Israel. Although Israel is a small country with a limited domestic market, it is important to China because of its advanced technology in electronics and several other sectors. Since the two countries established bilateral diplomatic relations in 1992, China has been eager to invest in Israel’s high-tech industry. Chinese firms have already invested in partnerships with Israeli firms active in cloud computing, artificial intelligence, semiconductors, and communication networks. An excellent example of these types of Chinese investments is the purchase of the Israeli telecommunications research firm Toga Network by the Chinese telecommunication giant Huawei in 2016.

As a result of these high-tech investments, China has emerged as one of the largest foreign investors in Israel’s equivalent to the Silicon Valley, conveniently called the Silicon Wadi. During 2014-2019 Chinese firms invested a sum of $1.5 billion in 300 Israeli hi-tech firms. Surprisingly, the United States’ restrictions on Chinese investments in the US have redirected some of these investors to Israel. At the same time, Israel is coming under increased US pressure to cut back its technological relations with China.

Many Israeli high-tech companies have investment partnerships with US firms and share some advanced technologies. As a result of the growing technological competition between the US and China, the US government is worried about transferring these technologies to Chinese firms that invest in Israel. It is also concerned that Chinese entities in Israel will engage in digital espionage for the Chinese government. Since the US is the primary defense and strategic supporter of Israel, the Israeli government is taking US sensitivities into consideration as it continues its investment and trade partnership with China. These considerations, for example, discouraged Israel from selecting Huawei, which is the world’s leading firm in 5G telecommunication technology, to develop Israel’s 5G network. Similarly, the Israeli government bypassed the Chinese firm CK Hutchison Group to develop the $1.5 billion Sorek B desalination plant in 2020, even though this firm had partnered with an Israeli firm for the construction of Sorek A desalination plant in 2011.

In addition to the United States, some Israeli national security officials have also raised the alarm about the risks associated with Chinese investments. Ever since 2017, several members of the Knesset have expressed concern about China, and the Knesset launched a classified hearing about this issue in July 2018. In January 2019, the head of Israel’s General Security Services (Shin Bet) called for increased monitoring of foreign investment. These concerns motivated the Israeli government to create a special committee in October 2019 to evaluate the security implications of foreign investment. It was broadly understood in Israel that the main target of these measures was China.

Overall, Israel has welcomed Chinese investments in many projects for more than two decades, and Israeli public opinion toward China has been favorable[vi]. In addition to significant investments in Israel’s high-tech sector and agriculture, Chinese firms are also active in several infrastructure projects. As of 2020, Chinese firms were involved in four such projects, including the construction of a new terminal in the port of Haifa and the expansion of the Ashdod port. Despite any potential risks and security concerns, the Israeli policymakers cannot ignore that Chinese firms are highly cost-effective and offer high-quality construction services. Moving forward, however, Israel-China economic relations will remain vulnerable to security concerns and US sensitivity. Concern about US sensitivities will also prevent Israel from signing a formal BRI agreement with China (similar to Egypt and Turkey).

Syria and Lebanon: Although China is already one of the largest exporters to both Syria and Lebanon, neither country has a suitable investment climate for China in the short run. China’s investments in Syria exceeded $4 billion before 2011, but it has made no new investments. China has a large tolerance for political instability and uncertainty. It has not hesitated to invest in countries like Sudan that other nations have cast aside because of violence and civil war. However, it invests in high-risk countries when the returns are high (such as production and extraction of mineral and oil resources) and justifies the risks.

Neither Syria nor Lebanon falls in this category because Syria’s oil exports are small, and some of them are located in areas that the Assad government does not control. Lebanon has recently discovered oil and natural reserves in the Mediterranean, but these discoveries are subject to an international dispute. Both countries have also been targets of US hostilities because of Hezbollah and the Assad regime’s close relations with Iran. Bashar Assad has survived the Syrian uprising with the help of Russia and Iran. Still, his government does not control many parts of the country, and Syria remains a target of severe economic sanctions and military interventions. Similarly, the US has imposed crippling financial sanctions on Lebanon (primarily because of the strong position of Hezbollah in that country’s power-sharing political system), and many blame these sanctions for the current disastrous economic conditions in that country.

Despite these adverse factors, China has expressed interest in providing infrastructure investment in both countries because of broader geo-economic and geopolitical considerations. Reconstruction of Syria’s infrastructure will positively affect China’s economic relations with Iran and Iraq. In recent years, China has deepened its economic relations with Iran and Iraq and has supported rail and highway connectivity among Iran, Iraq, and Syria. Iran is already connected to China’s BRI railway network that runs from China to Central Asia. Once these transportation networks are established, China will have an additional transportation link to Iraq and Iran through Syria.

Another factor encouraging China to invest in Syria and Lebanon is the rising geopolitical competition between the US and China. As the United States intensifies its efforts to reduce China’s influence around the world, China is showing more willingness to expand its relations with countries that are targets of American hostility and economic sanctions, such as Syria, Venezuela, and Iran. Furthermore, China has developed strong strategic coordination with Russia to challenge American influence in Central Asia and Middle Eastern countries such as Iran and Syria. This is evident in the frequent veto of anti-Syria resolutions in the United Nations by Russia and China. In the early stages of the Syrian conflict, China tried to maintain neutrality among the warring factions and support a political solution through peace negotiations. In this context, it has maintained good relations with the Assad regime. Economic reconstruction of Syria under the Assad Regime is a shared objective of Russia and China. At the same time, Chinese firms will face competition from Russian firms for investment opportunities in Syria because the Assad regime owes its survival to Russian support and is likely to show its appreciation by a positive bias toward Russian firms.

The Assad regime is eager to expand diplomatic and economic relations with China. Desperate for foreign investment, it actively seeks Chinese investment and has expressed readiness to join the Belt and Road initiative. Bashar Assad demonstrated this strong interest by hosting the Chinese foreign minister as his first meeting with a foreign dignitary immediately after his inauguration in July 2021. Among Lebanon’s political factions, Hezbollah has emerged as the leading advocate of “looking east” and welcoming Chinese investments, but as the economic crisis worsens, other politicians are also courting China.

Observations and regional analysis

Based on the above analysis, a bird’s eye view of China’s economic relations with Levant countries offers many observations about the direction and prospects of these relations.

Bilateral, not regional: In light of the weak or non-existent economic and diplomatic relations among most Levant countries, China’s relations with these countries have developed bilaterally and without any regional coordination. Like most regions of MENA, the relations among Levant countries are dominated by tension and conflict. China has accepted these tensions’ longevity and has focused on bilateral relations while maintaining neutrality. This lack of goodwill and cooperation among Levant neighbors will deny them the shared benefit of creating regional connectivity through BRI transportation infrastructure.

While each Levant country’s economic engagement with China (and potentially other countries outside the region) is expected to increase, there is little prospect that participation in BRI will contribute to regional economic integration. The required stability, peace, and political will for greater cooperation are still missing. Yet, participation in BRI may indirectly strengthen intra-Levant economic linkages by increasing economic prosperity. Take, for example, the case of Egypt and Turkey, which are both counting on engagement with China to accelerate their development and economic growth. Faster economic growth and improved investment climate will incentivize both countries to expand their economic and diplomatic relations.

Impact of the pandemic: The Covid-19 pandemic caused a severe but temporary disruption to China’s BRI projects all over the world as both China and many host countries were forced to divert BRI financial resources to medical care. The engagement of China with Levant countries since the start of the pandemic points to a continuation of China’s interest in the region. However, the aggregate value of Chinese investments in the area diminished in 2020. While many Chinese investment projects in Levant countries were suspended, China quickly offered pandemic-related assistance (masks, covid test kids…) to all Levant countries. This was partly a response to the medical supplies that some of these countries, such as Egypt and Israel, sent to China in the early stages of the pandemic, when it was causing a health crisis in China in February 2020, but had not reached the MENA region yet. By April 2020, the Chinese government sent masks and other medical supplies to all Levant countries as part of its worldwide pandemic assistance strategy. It also participated in joint projects to develop Covid tests and vaccine production with Egypt and Israel.

Moving beyond this initial sale and donation of medical equipment, China has continued its BRI engagement with Levant countries but has focused on new digital communications and healthcare projects, which had a higher priority for these countries for coping with the pandemic[vii]. This included projects by leading Chinese high-tech firms such as Huawei and ZTE to upgrade and expand the digital telecommunication capacity in Egypt and Turkey. China is also developing a joint vaccine production facility in Egypt to supply Covid-19 vaccines to Africa.

The US Pushback: The United States has not seized its concern about the reliance of its Middle East allies on Chinese advanced technology despite the pandemic. In addition to Israel, Egypt has also come under US pressure to avoid Chinese firms developing its 5G industry. These anti-Chinese campaigns are expected to be less effective in Egypt and Turkey, which have had tensions with Washington in recent years. Both Erdogan and El-Sisi consider China as a crucial economic partner that is indispensable for their respective economic development strategy. Since the United States still enjoys significant but varying degrees of leverage over Israel, Jordan, Egypt, Turkey, and even the fragmented Lebanon, these countries will occasionally find themself caught up in the middle of the US-China rivalry in the coming years.

I anticipate that China will try to remain focused on expanding its economic and technological relations with Levant countries without seeking military and strategic alliances against the US. The expansion of economic relations will include greater use of Chinese currency Renminbi (Yuan) for financial transactions with Levant countries. In recent years Turkey, Egypt, and Syria have taken steps to facilitate the Renminbi for trade with China.

Egypt vs. Turkey: While the current political leadership of Egypt and Turkey are both trying to expand their relations with China, there is some level of substitution and competition between their roles in China’s BRI vision in the Eastern Mediterranean. They are both large economies with a good supply of semi-skilled and skilled labor; and attractive commercial seaports. They can both serve as manufacturing hubs and logistic transshipment cargo centers for BRI. Looking at China’s engagement with Turkey and Egypt in the past ten years, it appears that while economic relations with both countries have expanded, Egypt is moving ahead and positioning itself as the main manufacturing and logistic hub for Chinese firms in the Mediterranean region.

This implies that some potential Chinese investments in Turkey might be ignored in favor of Egypt. The role of Turkey in the BRI will hence be more limited to middle corridor transportation and transshipment to Eastern Europe. On the other hand, Egypt will play a broader role in China’s global transportation and production supply chain. In manufacturing activities, Chinese investments in Turkey will focus on select (relatively more advanced) sectors such as telecommunication and joint development of advanced weapon systems, while Egypt will attract a broader range of Chinese manufacturing investments, which will produce a more diverse range of products.

Several factors are contributing to these differences in Egypt and Turkey’s economic engagements with China. One possible factor for Egypt’s advantage is that President El-Sisi has been more focused on creating a hospitable environment for Chinese investments. As mentioned earlier, in addition to Egypt’s geographic advantage, successive Egyptian regimes have remained consistent in their desire to preserve and expand their relations with China in the past two decades. They also invest in specific activities such as Chinese language education and China-sponsored vocational training programs to prepare Egyptian workers for employment in Chinese firms.

It also appears that the domestic political environment of Egypt is more stable under El-Sisi’s authoritarian rule. On the other hand, President Erdogan faces domestic opposition parties that are highly critical of some Chinese investments. If these parties fare well in future presidential or parliamentary elections, they might adopt less-friendly policies towards China. Egypt will also be a more attractive manufacturing hub for export products because it has fewer tensions in its foreign policy than Turkey. Turkey has had occasional tensions with the US, the European Union, Russia, several Arab countries, and Israel in the past decade. On the other hand, Egypt has pursued a rather conservative foreign policy, and as a result, it is more suitable for Chinese investors who are looking for a trade, logistics, and export hub.

A fourth factor that might make Egypt more attractive for Chinese firms is the difference in public opinion toward China in Egypt and Turkey. Recent public opinion surveys (2017-2018) in Middle Eastern countries have shown that respondents in Egypt have a more favorable opinion about China than Turkey. Furthermore, because of their strong cultural and linguistic links with the Uyghurs, the citizens of Turkey are more sensitive to China’s treatment of this ethnic minority than Egyptians. As a result, the Uyghur question will pose more political risks in China-Turkey relations than China-Egypt relations. Furthermore, there is more unpredictability in diplomatic maneuvers and alliance shifts of President Erdogan than Egypt’s President El-Sisi. In other words, Egypt is more likely to maintain stable and positive relations with the Eastern Mediterranean and Europe than Turkey. Hence, it might have more appeal to China as a regional BRI production and logistic hub.

Conclusion

In some regions of the world, such as southeast Asia or Eurasia, countries that participate in China’s Belt and Road Initiative develop strong economic links with China and develop stronger intra-regional economic linkages among themselves. This is not the case in the Levant region, and the relations among Levant countries are dominated by conflict, tension, and minimal levels of cross-border trade and investment.

Due to these intra-Levant conflicts, two east-west BRI transportation networks are likely to emerge in the Levant. China is supporting Turkey to develop the middle-corridor for land connection to Central Asia. Syria, Iraq, and Iran would like to develop cross-border highway and railroad connectivity with China’s help and, if developed, it will serve as the second Levant east-west corridor. This project, however, will face uncertainty because of the US and Israeli efforts to deny Iran land connectivity to Iraq and Syria. The Suez Canal will overshadow these land-based transportation links, as it will serve as the most critical BRI route in Eastern Mediterranean. In the meantime, all Levant countries will develop stronger bilateral economic ties with China.

The data and evidence suggest that among Levant countries, Egypt’s relations with China are expanding to a higher level than others, and the political leadership of both countries shows a strong commitment to bilateral relations. China is also actively courting President Erdogan and has offered him financial support for several of his mega-projects. Turkish-Chinese relations were adversely affected by the Chinese treatment of Uyghur Muslims up until five years ago. Still, President Erdogan strategically decided to suppress that issue for the sake of economic relations with China and the attraction of Chinese investment. This is a welcomed development by China, but some citizens and opposition political leaders in Turkey are still very sensitive about Uyghurs. These sentiments might affect bilateral relations in the future.

Israel-China economic relations were on track to expand rapidly, particularly in the hi-tech sector. Still, Israel has had to partially curtail some Chinese investments because of US concerns about Chinese access to advanced technologies and espionage. Other Levant countries are also likely to face US demands for limiting their dependence on Chinese technology and supply chain, but they are likely to be less cooperative than Israel. The United States has some leverage on Jordan, but it is not concerned about any strategic risks in Jordan-China relations.

With regards to Egypt and Turkey, on the other hand, the US has some reservations about the growing role of China, but it has limited leverage on the current political leadership of these countries. Syria, which under the Assad regime has been a target of American sanctions and military intervention, is eager to expand its relations with China for both economic and strategic reasons. In Lebanon’s fragmented political system, the Hizbollah actively advocates for close ties with China despite reservations from other political factions that prefer more intimate relations with the United States and Europe.

References

Abu Zeid, Adnon, “Iran Moving Forward with Railway Link to Syria via Iraq”, Al-Monitor, November 18, 2018.

“Amid US pressure, Israel taps Local Firm over China for $1.5 b desalination plant”, Times of Israel, May 26, 2020.

Azhari, Timour, “US Caesar Act Could Bleed Lebanon for Years to Come”, June 19, 2020.

Burton, Guy. “Public Opinion in the Middle East towards China”, Middle East Institute, December 11, 2018.

Clinch, Matt, “China backs Turkey to overcome its economic crisis”, CNBC, August 17, 2018, (Online citation: September, 4, 2021).

“Case Study: Hunutlu EMBA Coal Plant”, March 23, 2021, Ranforect Action Network.

Calabrese, John, “China and Syria: In War and Reconstruction”, Middle East Institute, July 9, 2019.

Colakoğlu, Selçuk, “Turkey-China Relations: From ‘Strategic Cooperation’ to ‘Strategic Partnership’?” Middle East Institute, March 20, 2018.

Chulov, Martin, “Syrian Economy Lies in Ruin and China Sniffs Opportunity”, The Guardian, July 21, 2021.

El-Tawil, Noha, “Why Egypt is Significant to belt and Road Initiative?”, Egypt Today, April 27, 2019,

Foot, Rosemary, “China’s Vetoes During the Syrian Conflict”, East Asia Forum, February 28, 2020,

Fouly, Mahnoud and al-Azrak, Emad, “Cooperating with China, Egypt eyes becoming regional hub for COVID-19 vaccine production”, Xinhua Net, September 7, 2021,

Gündüzyeli, Elif, “A Chinese Coal Plant Highlights Turkey’s Flawed Energy Policy”, China Dialogue, September 3, 2020,

Gonzalez, Ricard, “China Harnesses ‘Health Diplomacy’ to Strengthen Foothold in the Middle East”, Equal Times, July 14, 2021.

Jizhong, Z, R. Ring, C. Jeffery, “The Belt and Road Initiative 2021 Survey: The Impact of Covid-19 on the BRI”, Central Banking, June 1, 2021.

Observatory of Economic Complexity, Datawheel.

Parsa, Mani, “Lebanon and Its Hezbollah Follow Iran, Hoping for a Chinese Rescue”, Radio Farda, July 16, 2020.

Ravel, Hagar, “How Will Increased Chinese Funding Affect Israeli Entrepreneurs?”, CTECH, October 24, 2019.

Sawers, Paul, “Huawei Reportedly Acquires Israeli IT Networking Company, TOGA Networks for $150 million”, Venture Beat, December 7, 2016.

“Syrian Parliament Okats Russian Lease of Tartus port”, France 24, December 6, 2019.

“Turkish Central Bank Says Used Chinese Yuan Funding for the First Time”, Reuters, June 19, 2020.

Notes

[i] These were needed to facilitate China’s rapid industrial development which began in the 1980s.

[ii] China’s annual investment in MENA declined from $25.2 billion in 2018 to $5.8 billion in 2020 (Calculated by author from China Global Investment Tracker database.) https://www.aei.org/china-global-investment-tracker/ .

[iii] The diplomatic relations between Egypt and China are much older and Jamal Abdul Nasser was the first Arab leader that diplomatic relations with China in 1956.

[iv] China and Egypt initially discussed the idea of Suez Economic Zone in 1990s but the project began in 2008. The Tianjin TEDA Compony has played an active role in development of this project ever since.

[v] The TEDA-Suez project is located in the southern sector of the Suez Canal corridor, near al-Shokhna and its development began in 2015.

[vi] According to a 2018 opinion survey about attitudes toward China in Middle Eastern countries, among Levant countries the favorable opinion toward China was high in Egypt and Israel, but low in Turkey.

[vii] China has labeled these new BRI priorities as Digital Silk Road and Health Silk Road.

Nader Habibi, Prof. Dr., Brandeis University’s Crown Center for Middle East Studies

Nader Habibi is the Henry J. Leir Professor of Practice in the Economics of the Middle East at Brandeis University’s Crown Center for Middle East Studies. Before joining Brandeis University in June 2007, he served as managing director of economic forecasting and risk analysis for Middle East and North Africa in Global Insight Ltd. Mr. Habibi has worked in academic and research institutions in Iran, Turkey and the United States since 1987. He earned his PhD in Economics from Michigan State University. His most recent research projects are: a) Economic relations of Middle Eastern countries with China, b) analysis of the excess supply of college graduates in Middle Eastern countries, c) impact of economic sanctions on Iranian economy. Habibi also served as director of Islamic and Middle East Studies at Brandeis University (August 2014-August 2019). He has published a work of fiction about Middle East geopolitics titled: Three Stories One Middle East (2014). Links to his publications are available at https://naderhabibi.blogspot.com/.

To cite this work: Nader Habibi, “China’s Economic and Strategic Relations with the Levant Region”, Panorama, Online, 9 November 2021, https://www.uikpanorama.com/blog/2021/11/09/chinas-economic-and-strategic-relations-with-the-levant-region

Copyright@UIKPanorama.All on-line and print rights reserved. Opinions expressed in this work belongs to the author(s) alone, and do not imply endorsement by the IRCT, the Editorial Board or the editors of the Panorama.